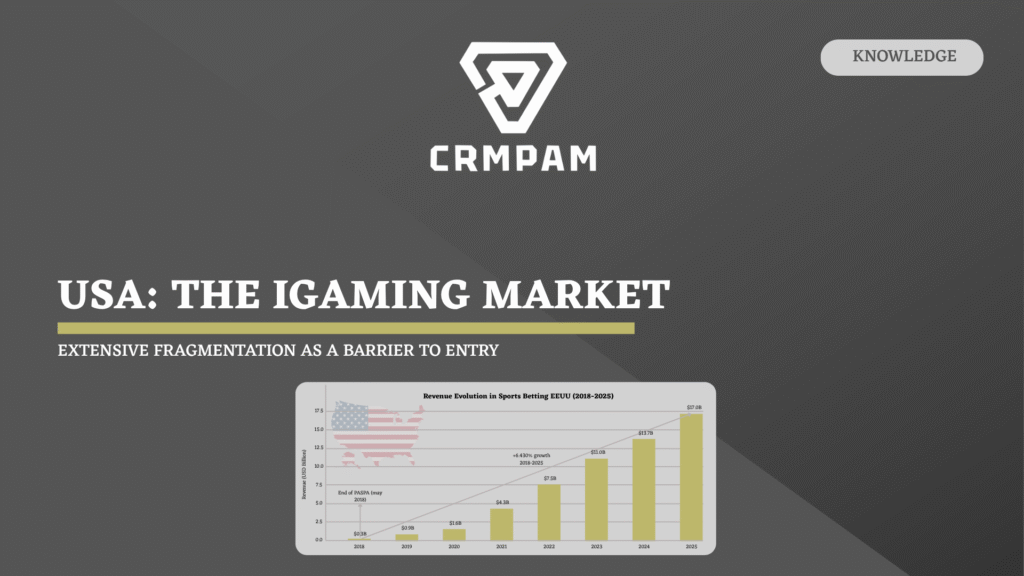

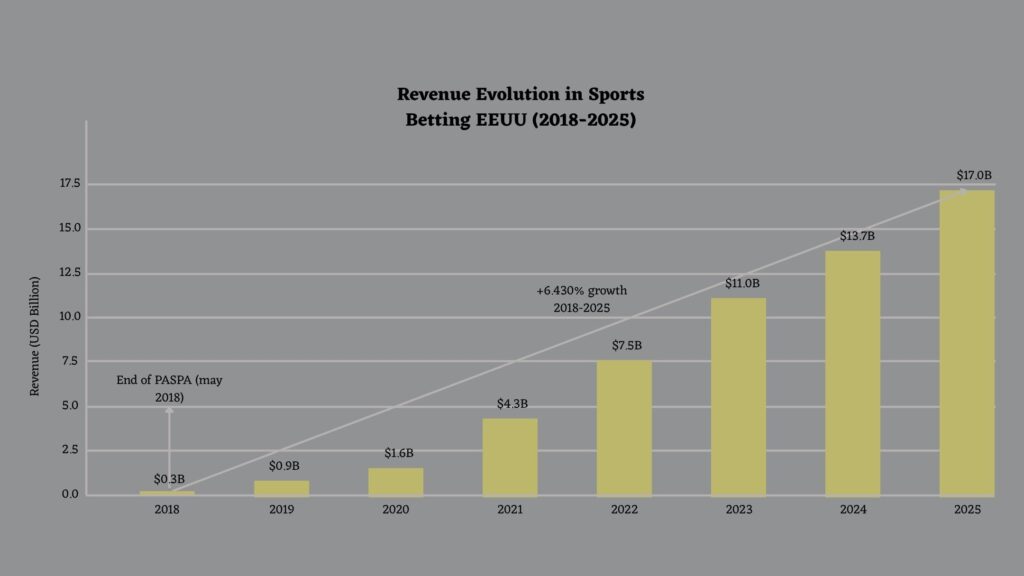

The United States until 2018 was a fairly anomalous market. While Europe, Asia and LATAM had decades of regulated sports betting markets, the country with the largest professional sports ecosystem in the world maintained a federal prohibition that made any bet outside Nevada an illegal act. The result was evident: a black market estimated at 150 billion dollars annually.

Today, the legal sports betting market in the USA generates $17.08 billion in annual revenue (2025), with a growth of +22.8% compared to the previous year, and iGaming (online casino) adds another $10.74 billion (+27.4% YoY).

The most striking figure is not the total volume, but the speed of construction: in 2018 the legal market generated barely $260 million, and in 2025 it is $17 billion.

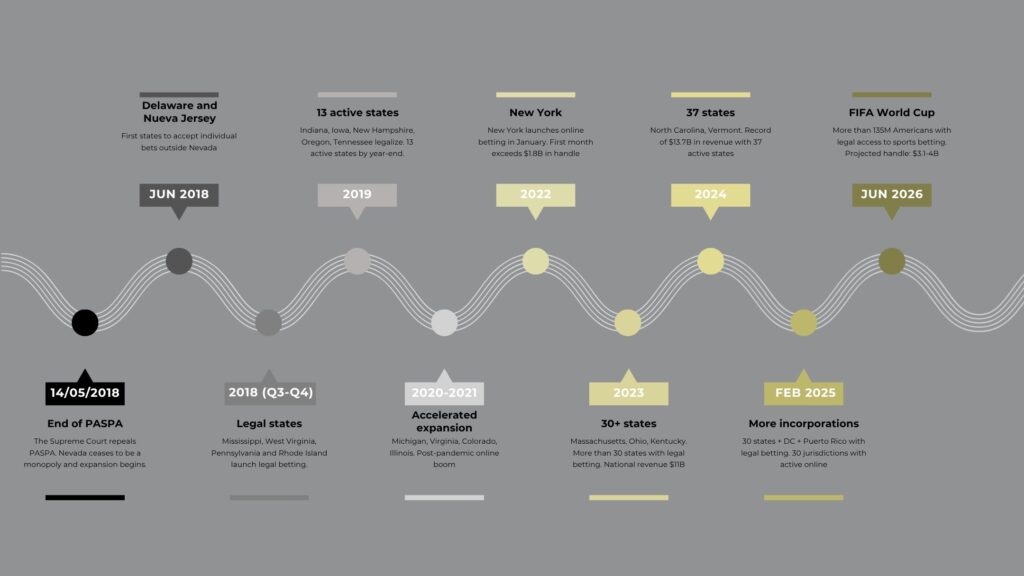

Post-PASPA regulation: The decision that changed everything

The Professional and Amateur Sports Protection Act (PASPA), enacted in 1992, had a central argument: sports betting corrupted the integrity of sport. Its practical effect was to make Nevada the legal monopoly of sports betting in the USA, while the rest of the country operated in the illegal market.

On May 14, 2018, the Supreme Court repealed PASPA and therefore Nevada ceased to be a monopoly and the expansion began.

Unlike European markets with centralized regulation, the USA has developed a state-by-state regulation model, which generates unique technical and operational complexity. Each state has its own regulatory body, its own tax rates (from 6.75% in Nevada to 51% in New York), its own geolocation requirements, restrictions, KYC, etc.

The American player: Behaviour and psychology

Understanding the bettor is fundamental for any technology provider that wants to operate in this market. Their profile differs significantly from the European or Latin American one, both in the sports they bet on, the formats they prefer and their relationship with technology.

The data points to a predominantly male bettor (>70%), with an average age of around 35–40 years, employed full-time and with above-average income.

Mobile First: Non-negotiable standard

In states with active online betting, 80–90% of the total handle is generated from mobile. This figure has only grown since 2018, when New Jersey reported that 75% of its first online bets came from mobile devices. The implication for technology providers is clear: any platform that is not optimized for mobile-first is not competitive in the American market.

Preferred formats and sports

One of the characteristic phenomena of the American bettor is combined bets, and especially the Same Game Parlay (SGP), which allows combining multiple markets in a single bet.

The favorite sports of American players are the NFL (dominating handle and revenue), the NBA (highest CAGR 2025–2030, greater adoption among young bettors), MLB (high frequency, ideal for props and microbets), Soccer (rapidly on the rise), MMA / Boxing (bettors with a more advanced profile, high demand for props).

Payment Methods: The financial ecosystem of iGaming

The payments ecosystem in American iGaming has peculiarities that do not exist in any other market in the world. The combination of the Wire Transfer Act, the Unlawful Internet Gambling Enforcement and the individual policies of banks create unique frictions in deposit and withdrawal processes that technology providers must contemplate in their infrastructure from day one.

| Method | Type | Acceptance | Deposit | Withdrawal | Note |

| ACH / VIP Preferred | Bank transfer | High | Instant (VIP) 1-3 days (standard) | 2-5 days | Favorite of high-volume bettors |

| PayPal | eWallet | High | Instant | Instant | Fast withdrawals |

| Venmo | P2P / eWallet | Medium | Instant | Instant | Owned by PayPal |

| Credit/debit card | Card | High | Instant | Not available | Withdrawals not allowed back to card |

| Crypto | Crypto | Low | Variable | Variable | Marginal method |

Unlike Europe, where eWallets are integrated into the standard flow, in the USA the withdrawal of funds is significantly slower. 84% of American bettors declare being more satisfied when withdrawals are instant, and fast withdrawals are the second most important factor for choosing a sportsbook, according to Paysafe.

For an iGaming platform provider, this means that the payment integration architecture must contemplate from day one a minimum of 4–5 payment methods to be competitive, with geolocation management per state and specific connectors with American processors such as Sightline Payments (VIP Preferred), Trustly and PayNearMe.

Conclusions: What this market demands

The USA is the market that is redefining global industry standards in growth speed, mobile adoption, innovation in betting formats and regulatory complexity.

- The size justifies the complexity: $16.96B in sports betting + $10.74B in iGaming in 2025. CAGR of 10.9% until 2030. No other market in the world offers this combination of volume and growth in such a clear time horizon.

- Fragmentation is the barrier to entry: 30 active regulatory configurations, each with its own requirements. Platforms that cannot be configured per market without touching the core are de facto excluded from operating at national scale.

- Mobile is the main channel: 80–90% of the handle comes from mobile devices. Without a first-class mobile experience, there is no product in the American market.

- Live betting is the technical frontier: 44% of the 2026 World Cup handle will be in-play. The ability to manage real-time odds updates under extreme traffic differentiates first-generation platforms from those that can compete in 2026.

- Payment defines retention: 88% of bettors would switch sportsbooks after a bad payment experience. An incomplete payment integration (without ACH/VIP Preferred, without PayPal) is not an inconvenience: it is a direct cause of customer loss.

CRMPAM – The quiet power behind your wildest traffic